(1)")

If you as a shareholder of the company owned 200 shares, you would then own an 20 additional shares, or a total of 220 (200 + (0.10 x 200)) shares once the company declares the stock dividend. Management knows that shareholders prefer receiving dividends, but they may not distribute dividends to stockholders. If they are confident that this surplus income can be reinvested in the business, then it can create more value for the stockholders by generating higher returns.

Step 2 of 3

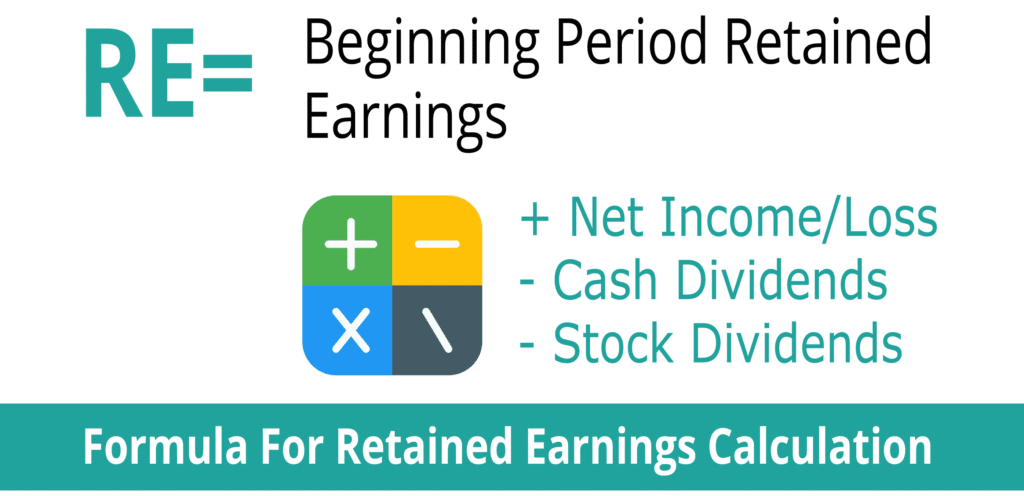

This amount represents the company’s profits that have been reinvested in the business. Retained earnings represent a useful link between the income statement and the balance sheet, as they are recorded under shareholders’ equity, which connects the two statements. This reinvestment into the company aims to achieve even more earnings in the future. Retained Earnings (RE) are the accumulated portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business.

What is the formula for the retained earnings ratio?

Revenue is the income a company generates from business operations during a period, while retained earnings are the accumulated net income that was not paid out as dividends to shareholders to date. Retained earnings are an accounting measure, representing the portion of profits not distributed to shareholders. However, it’s essential to understand that these earnings may not necessarily reflect the company’s available cash. Companies can reinvest these earnings in non-cash assets or operations, making it important to assess the company’s cash flow separately. In financial modeling, it’s necessary to have a separate schedule for modeling retained earnings. The schedule uses a corkscrew-type calculation, where the current period opening balance is equal to the prior period closing balance.

What is a statement of retained earnings?

Management, on the other hand, will often prefers to reinvest surplus earnings in the business. This is because reinvestment of surplus earnings in the profitable investment avenues means increased future earnings for the company, eventually leading to increased future dividends. A company that routinely gives dividends to shareholders will tend to have lower retained earnings, and vice versa. In an accounting cycle, after a trial balance and adjusting and closing entries are completed, and the income statement is generated, we are ready to prepare the Statement of Retained Earnings. No, Retained Earnings represent the cumulative profit a company has saved over time. Retained earnings are one of the options available to a company’s shareholders when distributing profits at the end of an accounting period.

- Recovering from negative retained earnings is not easy, but it is possible with the right approach and willingness to make tough decisions.

- Accumulated earnings, as they are also known, are a liability since it is an unfulfilled obligation to the owners.

- This is the net profit or loss figure from the current accounting period, from which the retained earnings amount is calculated.

In the world of finance, understanding Retained Earnings is crucial for investors and business owners alike. This financial term holds the key to a company’s financial health and growth prospects. In this article, we’ll negative retained earnings delve into the fundamentals of Retained Earnings, explaining what it is, how to calculate it, and why it matters. A company’s shareholder equity is calculated by subtracting total liabilities from its total assets.

Determine Beginning Retained Earnings Balance

As such, some firms debited contingency losses to the appropriation and did not report them on the income statement. To better explain the retained earnings calculation, we’ll use a realistic retained earnings example. Let’s say that a marketer named Elena is looking to expand her agency, but needs to provide some information about retained earnings to attract new investment.

He is an expert on personal finance, corporate finance and real estate and has assisted thousands of clients in meeting their financial goals over his career. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. GAAP specifically prohibits this practice and requires that any appropriations of RE appear as part of stockholders’ equity.

Retained earnings provide insights into a company’s historical profitability and its policy on dividend distribution. They also offer a gauge for the amount of funds that have been reinvested into the company. Analysts and investors scrutinize this financial metric to assess the firm’s financial stability and growth potential. A consistent increase in retained earnings typically suggests a company with a strong profit-making ability, whereas a decrease could indicate potential trouble or a deliberate strategy of heavy investment. Dividends paid are the cash and stock dividends paid to the stockholders of your company during an accounting period. Where cash dividends are paid out in cash on a per-share basis, stock dividends are dividends given in the form of additional shares as fractions per existing shares.